Institutional Insights: Societe Genrale - ETF Positioning

ETF Flows: Cautious Rebuild, Not a Full Risk-On Reset

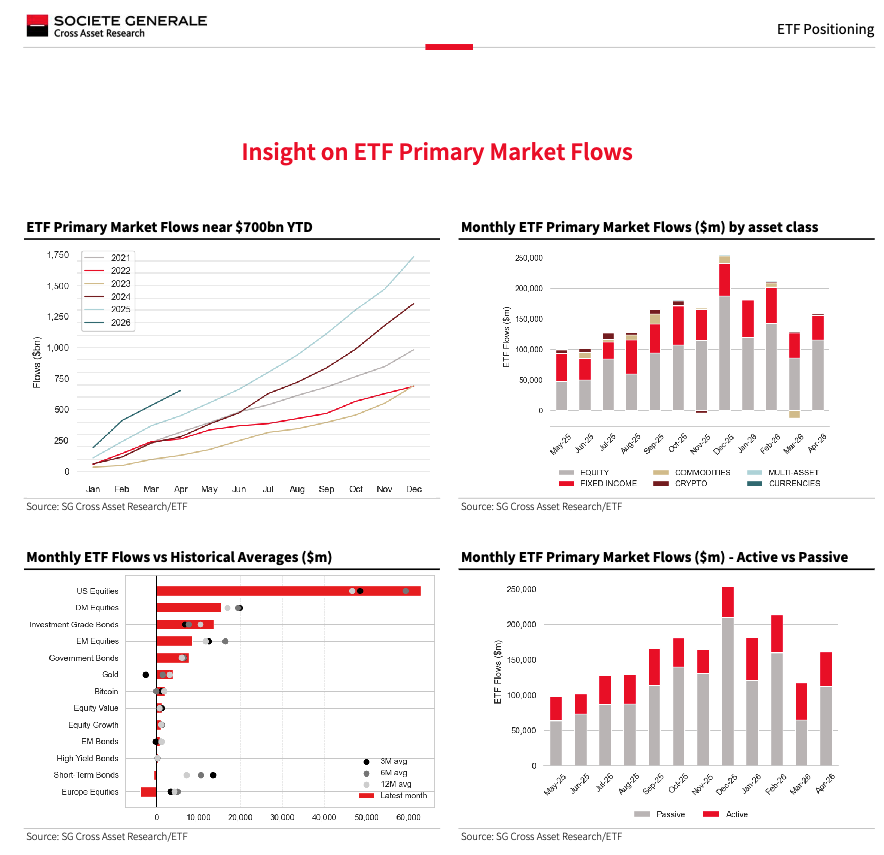

April ETF flows show a partial recovery in risk appetite after March’s war-driven de-risking, but the rebound was still selective rather than euphoric. YTD ETF primary-market flows are now running near $700bn, and April saw investors reallocate back into areas that had been sold during the March shock: US equities, investment grade credit, high yield, EM debt and gold all returned to net creations. The message is not that investors have dismissed Middle East risk, but that they are willing to rebuild exposure where the macro/earnings story remains credible and where liquidity is deepest. The strongest equity preference remains the US, supported by resilient earnings expectations and momentum positioning, while Japan also attracted inflows as the weaker yen helped sentiment for most of the month. By contrast, Europe saw its first monthly equity ETF redemptions in several months, reflecting weaker growth expectations, energy sensitivity and reduced confidence amid the prolonged geopolitical crisis and Hormuz disruption.

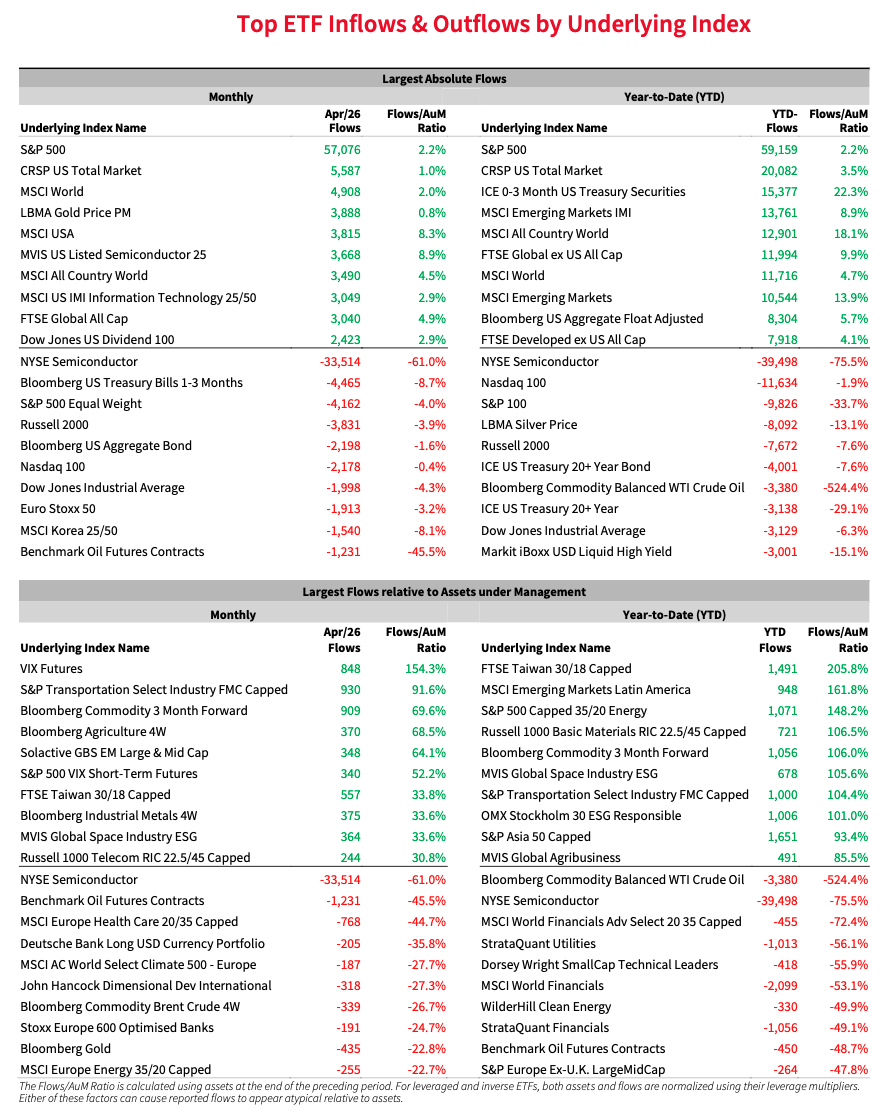

The equity flow picture is therefore highly regional and thematic. US equity inflows are still the clearest sign of the “earnings resilience plus secular growth” trade, while Japan keeps benefiting from FX-assisted equity appeal even with the risk of late-month yen intervention. EM was more differentiated than broadly risk-on: China onshore and Taiwan returned to inflows on valuation and tech-cycle support, while Brazil benefited from commodity and real-asset exposure. Thematic flows also tell an important story: investors continued to allocate to clean energy and real assets, suggesting structural themes still have sponsorship even in a less certain macro backdrop. At the same time, energy sector equity ETFs saw their first net outflow after seven months of inflows, an important positioning inflection. That may reflect profit-taking after the oil spike, some de-escalation expectations, or a view that the market has already expressed the easier geopolitical-energy trade.

In fixed income, the key shift was a move out of defensive cash-like positioning and back into spread products. Investment grade and high yield corporate bond ETFs returned to inflows, alongside renewed demand for EM debt. Short-duration and cash-like bond exposures saw selling pressure, suggesting investors were reducing crisis hedges and redeploying into carry. Currency allocation was also notable: investors sold GBP-denominated bond exposures while increasing allocations to USD-denominated fixed income, consistent with the dollar’s yield advantage and safe-asset demand. Gold flows turned modestly positive at around +$4bn, while Bitcoin saw a second consecutive month of inflows at roughly +$2bn, pointing to selective alternative allocation rather than a blanket risk-on or risk-off posture.

The strategy-level flows show investors are rebuilding risk but still hedging the tails. VIX futures-linked products attracted strong inflows, which suggests investors are not abandoning protection even as equity and credit flows recover. Cyclical and economically sensitive exposures, including transportation strategies, also saw renewed demand, consistent with the improvement in risk appetite. But leveraged ETFs saw meaningful redemptions, led by outflows from ProShares UltraPro QQQ and Direxion Daily Semiconductor Bull 3X Shares, likely reflecting profit-taking after April’s very strong benchmark performance, with the NASDAQ-100 up around 15% and the NYSE Semiconductor Index up around 40%. This should not be overread as bearish tech sentiment; leveraged ETF flows are tactical and often driven by rebalancing, volatility dynamics and derivatives positioning. Still, it does show investors are more willing to take profits in crowded high-beta expressions while retaining core US equity and tech exposure.

Trading takeaway: April ETF flows argue for a cautious risk rebuild, not a clean all-in risk-on rotation. The market is adding back exposure to US equities, credit, EM debt and alternatives, but the simultaneous inflows into VIX-linked products and outflows from leveraged tech ETFs show investors still want protection and are reducing the most aggressive beta. Regionally, stay overweight US over Europe, with Japan still supported but more vulnerable to yen intervention. In fixed income, the flow impulse favors credit over cash-like duration hedges, especially IG and selective HY. In commodities/alternatives, gold and Bitcoin flows are still positive, while energy equity outflows suggest the sector may need new oil/geopolitical confirmation to speed up again. The bottom line: investors are rebuilding risk exposure, but they are doing it with hedges on, and that supports a market of selective upside, persistent dispersion and continued demand for volatility protection.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!