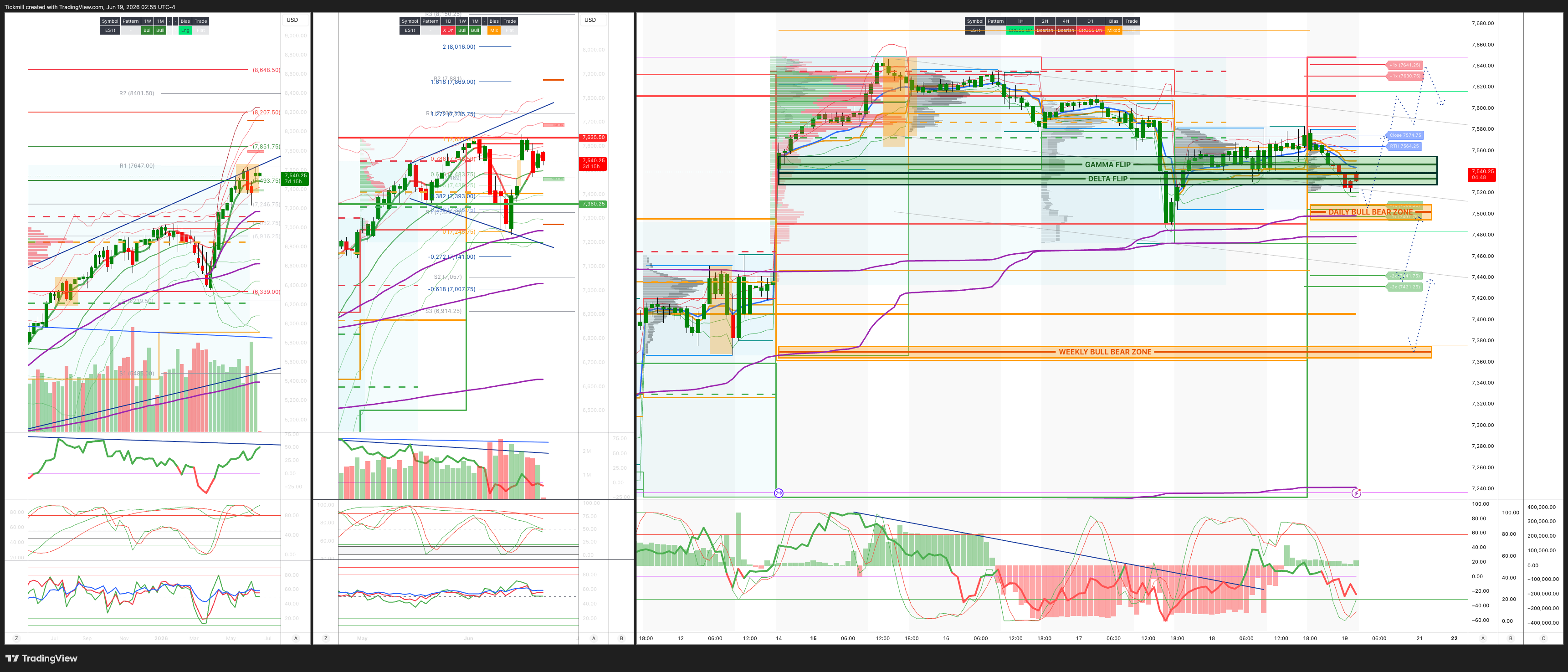

S&P500 Daily Action Areas & Price Targets 19/6/26

S&P500 Daily Action Areas & Price Targets 19/6/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7365/75

WEEKLY RANGE RES 7635 SUP 7360

MONTHLY RANGE RES 7932 SUP 7384

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.28 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BEARISH 7571

WEEKLY VWAP BEARISH 7474

MONTHLY VWAP BULLISH 7036

DAILY STRUCTURE - OTFL - 7604

WEEKLY STRUCTURE - OTFH

MONTHLY STRUCTURE - OTFH - 7199

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7580/90

GAMMA FLIP 7547

DELTA FLIP 7534

DAILY RANGE RES 7642 SUP 7508

2 SIGMA RES 7710 SUP 7438

VIX BULL BEAR ZONE 17.4

TRADES & TARGETS

LONG ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET RTH CLOSE

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Flows & Positioning Into The Holiday Weekend’

Markets are round-tripping the Warsh/FOMC hawkish shock overnight, with Asia AI, semis, and hardware names back in leadership. The message from Korea and Japan remains “more capex, more spend, more demand,” and anything tied to the AI buildout continues to attract capital. SK Hynix making new highs and rallying 7% is the cleanest signal that the market still wants to own the picks-and-shovels side of AI, especially memory and HBM, even as the broader AI economics debate becomes more complicated. At the same time, MSCI China falling 20% from its October high and moving into bear-market territory is a major divergence: the global AI/capex cycle is supporting North Asia hardware, while China remains stuck in a separate macro, policy, and confidence problem.

Oil is again the main macro release valve. The newly visible details of the signed 14-point MOU suggest the framework has been deliberately engineered to take maximum pressure off crude. Based on what has been reported, it accommodates several of Iran’s key demands, including retention of its ballistic missile program, no requirement to export enriched uranium, access to frozen assets, and a large reconstruction package around $300bn. There are still obvious questions around implementation, sequencing, verification, and political durability, but the market is focused on the near-term implication: regional security and nuclear disputes have effectively been delayed, deferred, or reframed in a way that reduces immediate supply-risk premium.

This matters because the oil selloff is bailing out equities from a more hawkish Fed. Warsh’s debut was clearly interpreted hawkishly, and GIR’s read captured the surprise: nine participants projected a hike in 2026 versus expectations for only three, while the median projection for 2027 Q4/Q4 core PCE inflation rose to 2.5% versus expectations of 2.3%. Market pricing for the end-2026 fed funds rate rose around 20bps after the projections and press conference. In a vacuum, that should be a clear headwind for equities. But lower oil offsets part of the inflation concern, supports consumers and margins, and allows the market to look through some of the front-end repricing.

Warsh’s reluctance to provide forward guidance drove a meaningful curve flattening. That is important because it suggests the market is not simply pricing a higher long-run nominal growth regime; it is pricing a less predictable and potentially more reactive Fed. A chair who avoids guidance creates more data dependence, more meeting-by-meeting risk, and more sensitivity to inflation prints. Some of that pricing may get walked back over the next few weeks, especially if oil continues falling and inflation data soften, but the initial message was undeniably hawkish relative to already hawkish expectations. For equities, the impressive part is how well the shock has been absorbed.

The open-source AI developments are the most important fundamental wrinkle. GLM-5.2, another Chinese open-source model, appears highly competitive on SWE benchmarks relative to recent private models. It is not quite frontier-leading, but the gap between open and closed models continues to narrow. The fact that weights are open under an MIT license and that the model can be distilled, quantized, and reproduced matters more than any single benchmark. It means capability diffusion is accelerating and competitive pressure on closed-model economics is intensifying.

Microsoft actively evaluating a self-hosted and fine-tuned version of DeepSeek V4 for Copilot compounds that pressure. If large enterprise distribution platforms can increasingly use self-hosted, fine-tuned, or open-weight models, token pricing power becomes harder to defend. Even if total usage grows dramatically, the marginal price per unit of intelligence may keep falling. This is the core tension in AI equities: adoption is booming, but monetization per token may compress faster than expected.

VibeThinker-3B is arguably more conceptually important than the benchmark headlines. The “Parametric Compression-Coverage Hypothesis” argues that reasoning is increasingly compressible, while knowledge remains a coverage problem. Put differently, solving a math or coding problem may require far fewer parameters than storing and retrieving broad factual knowledge. If that is true, the industry may be underestimating how much useful reasoning can migrate into smaller, cheaper, and increasingly local models.

The implication is a bifurcated AI architecture. Frontier models will still matter when users need frontier capabilities, the broadest knowledge coverage, the highest reliability, or complex multimodal reasoning. But open and local models may handle a growing share of everyday tasks, especially if 3B-class reasoning models can run on standard consumer laptops or edge devices. That does not eliminate compute demand; it changes where inference happens and who captures value. The frontier remains compute-hungry, but the addressable pool of tasks that can be done locally appears to be expanding rapidly.

For hyperscalers, this is both a demand story and a margin-risk story. They still appear convinced they must keep spending to remain competitive, and no one wants to be the first to blink if AGI or frontier-level advantage remains within reach. But token-cost compression, open-source models, self-hosted enterprise deployments, and neocloud competition all put pressure on the pricing side of the equation. If falling compute costs and falling token prices pass through to customers faster than providers can monetize incremental usage, the benefits accrue more to users than to hyperscaler shareholders.

The reflexivity point is critical. The capex cycle may not stall because demand disappears. It may stall because investors decide that the next dollar of spend no longer earns an attractive incremental return. Ironically, the first hyperscaler to credibly signal that it can slow spending while maintaining product quality may be rewarded by the market. If that happens, peers will notice, and the competitive equilibrium could shift from “spend at all costs” to “prove returns on spend.” Hyperscaler share prices are therefore a leading indicator for the durability of the AI capex cycle.

This is why the lack of market reaction to new open/local model progress is surprising. Investors continue to reward the physical buildout and have not materially changed spending outlooks; if anything, capex expectations keep moving higher. That may be correct if lower inference costs unlock vastly more usage and drive Jevons-style compute demand. But the market is not yet pricing much risk that token deflation and model commoditization reduce provider economics. For now, the equity market is treating open-source progress as adoption-positive rather than margin-negative.

US expiry adds a supportive technical backdrop. Institutional sentiment still feels subdued, even as retail sentiment is bordering on euphoric, helped by summer, the World Cup, and markets near highs. That split matters. Institutions remain cautious after the recent factor violence and Fed uncertainty, while retail is leaning into momentum and speculative leaders. This can keep the tape bid in the short run, but it also raises the risk of sharp air pockets if the retail-led pockets lose momentum.

The biggest risks remain AI-related disappointments and a more hawkish Fed. The Fed risk is clear: Warsh has introduced a higher and less predictable policy floor, and the market is now more exposed to upside inflation surprises. The AI risk is subtler: the market is still extrapolating capex growth and infrastructure demand, but open-source/local model progress and token deflation are moving quickly. If hyperscaler stocks begin underperforming persistently despite rising capex, that would be the warning that investors are shifting from “more spend means more growth” to “more spend means lower returns.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!