Another dovish surprise in US PPI boosts stocks and bonds, pressures USD

Citing significant economic uncertainty in the coming months, OPEC has lowered its oil consumption growth forecast for the 5th consecutive time since April. The adjustment was -100K b/d for 2022 and 2023. The last time OPEC revised its forecast at the last meeting, it was decided to increase production by 2 million barrels per day. Among the main reasons for the negative change in the forecast, OPEC mentioned economic challenges in Europe and the still tight covid restrictions in China, which make for quite an uncertain path to economic recovery for Beijing.

At the same time, OPEC believes that the faster than expected weakening of inflation will lead to a rebound in demand, as central banks will experience less pressure to tighten policy, and thus restrain the expansion of economies.

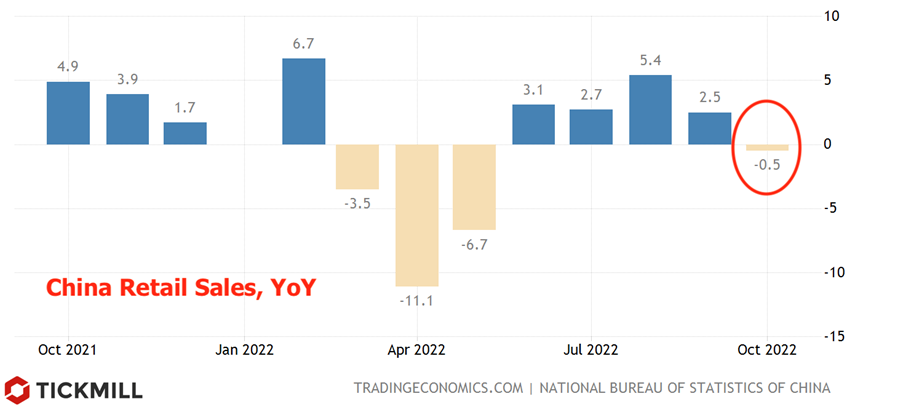

Data on Tuesday showed retail sales in China fell 0.5% year-on-year, while industrial production growth fell short of expectations:

Together with the weak foreign trade data (YoY contraction of imports and exports in October), this raises the likelihood that the CCP will prepare new economic stimulus measures and move towards a systematic easing of covid restrictions. In my view, upside potential on positive stimulus news from China remains high.

Japan's GDP unexpectedly contracted in the third quarter, which added to the negative for the yen. However, a broad dollar retreat took over and USDJPY is down half a percent today.

European markets rose moderately, futures for US indices advanced through key resistance levels. The S&P 500 futures topped 4,000 after dovish US PPI report, which, like consumer inflation, surprised on the downside. The dollar collapsed on the data, indicating high sensitivity of the market to data on inflation pressures in the US:

Producer prices rose only by 0.2% m/m against the forecast of 0.4%, which was another argument in favor of the fact that the general trend of inflation in the US is now downward and the US Central Bank will soon move to softer rhetoric and policy actions.

For the British economy, the unemployment report came in worse than expected, the increase in the number of unemployed in October was twice as high as the forecast, while the average wage accelerated to 6% YoY (5.9% forecast).

The index of economic sentiment from ZEW in Germany turned out to be higher than expected, the index in October amounted to -36.7 against the forecast of -50 points. In the previous month, the reading was near the all-time low of -59.2 points.

The markets continue to price in an inflation slowdown in the US and cut excessive dollar cash longs on the US dollar, anticipating a dovish policy turn by the Fed in December. Bullish momentum in risk assets and bonds and downward pressure on USD will likely be extended in the run up to the upcoming FOMC decision.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.